Leasing a car typically costs between $300 and $800 per month, depending on the vehicle, down payment, and lease terms. This guide breaks down all the factors that influence lease pricing and offers practical tips to help you get the best deal.

In This Article

- 1 Key Takeaways

- 2 How Much Does It Cost to Lease a Car?

- 3 What Determines the Cost of a Car Lease?

- 4 Average Lease Prices by Vehicle Type

- 5 Hidden Costs and Fees to Watch Out For

- 6 How to Get the Best Lease Deal

- 7 Leasing vs. Buying: Which Is Cheaper?

- 8 Final Thoughts: Is Leasing Right for You?

- 9 Key Takeaways

- 10 Frequently Asked Questions

Key Takeaways

- Monthly lease payments range from $300 to $800: Most drivers pay between $300 and $800 per month, with luxury and high-end models costing more.

- Down payments reduce monthly costs: A larger down payment (cap cost reduction) lowers your monthly payment but increases upfront expenses.

- Credit score impacts lease rates: Borrowers with excellent credit (720+) typically qualify for lower interest rates (money factors).

- Mileage limits affect pricing: Standard leases allow 10,000–15,000 miles per year; exceeding this results in per-mile fees.

- Lease term length matters: Shorter leases (24–36 months) often have higher monthly payments but lower total cost.

- Depreciation drives lease costs: Since you’re paying for the car’s drop in value during the lease, newer or faster-depreciating models cost more.

- Negotiate the capitalized cost: Just like buying, you can negotiate the car’s price to lower your lease payment.

[FEATURED_IMAGE_PLACEHOLDER]

How Much Does It Cost to Lease a Car?

Thinking about leasing a car? You’re not alone. Leasing has become a popular alternative to buying, especially for drivers who want lower monthly payments, the latest technology, and the ability to drive a new vehicle every few years. But before you sign on the dotted line, it’s important to understand exactly how much it costs to lease a car—and what factors influence that price.

So, how much does it really cost? On average, most people pay between $300 and $800 per month to lease a car. That’s a wide range, and the final number depends on several key factors, including the type of vehicle, your credit score, the length of the lease, and how much you’re willing to pay upfront. For example, leasing a compact sedan like a Honda Civic might cost around $250 to $350 per month, while leasing a luxury SUV like a BMW X5 could run $700 to $1,000 or more. But those are just averages. The real cost comes down to the details—and knowing how to navigate them can save you hundreds, even thousands, over the life of your lease.

What Determines the Cost of a Car Lease?

Leasing isn’t just about picking a car and signing a contract. The price you pay each month is calculated using a formula that considers several financial and contractual elements. Understanding these components will help you make smarter decisions and avoid overpaying.

Depreciation: The Biggest Factor

The single biggest factor in your lease payment is depreciation—the amount the car loses in value during the lease term. When you lease, you’re essentially paying for the car’s drop in value from the time you drive it off the lot until the end of the lease. For example, if a new car costs $40,000 and is expected to be worth $24,000 after three years, you’re paying for that $16,000 loss in value, plus fees and interest.

Cars that depreciate quickly—like luxury brands or models with poor resale value—will have higher lease payments. On the flip side, vehicles with strong resale value, such as Toyota, Honda, or Subaru, often have lower monthly costs because they lose value more slowly.

Interest Rate (Money Factor)

Just like a loan, your lease includes an interest charge, known as the “money factor.” This is essentially the lease equivalent of an APR. It’s expressed as a small decimal (e.g., 0.00250), which you can convert to an approximate APR by multiplying by 2,400. So, 0.00250 × 2,400 = 6% APR.

Your credit score plays a major role here. Borrowers with excellent credit (720 or higher) typically qualify for the lowest money factors, sometimes as low as 0.00100 (2.4% APR). Those with fair or poor credit may face much higher rates, increasing their monthly payment significantly.

Lease Term Length

Lease terms usually range from 24 to 48 months, with 36 months being the most common. Shorter leases mean higher monthly payments because you’re paying off the depreciation in fewer months. However, shorter leases also mean you’re driving a newer car and may avoid major repair costs. Longer leases (48 months) spread the cost over more months, lowering the payment, but you may face higher wear-and-tear charges at the end.

Mileage Allowance

Most leases come with an annual mileage limit—typically 10,000, 12,000, or 15,000 miles. If you exceed this limit, you’ll be charged a per-mile fee, usually between $0.10 and $0.25. For example, driving 18,000 miles in a year on a 12,000-mile lease could cost you an extra $1,500.

If you know you’ll drive more than average, consider paying a little extra upfront for a higher mileage allowance. It’s often cheaper than paying overage fees later.

Down Payment (Cap Cost Reduction)

The down payment on a lease—called a “capitalized cost reduction”—directly reduces your monthly payment. For example, putting $3,000 down on a $40,000 car lowers the amount you’re financing, which reduces depreciation and interest charges.

However, a large down payment increases your upfront cost and puts more money at risk if the car is totaled or stolen. Many experts recommend minimizing the down payment and instead rolling any incentives or trade-in value into the lease to lower the monthly cost without tying up cash.

Average Lease Prices by Vehicle Type

Lease costs vary widely depending on the type of vehicle you choose. Here’s a breakdown of average monthly lease payments across different categories, based on current market data.

Compact and Economy Cars

These are the most affordable options to lease, ideal for budget-conscious drivers or those with short commutes. Examples include the Honda Civic, Toyota Corolla, and Hyundai Elantra.

– Average monthly payment: $250–$350

– Typical lease term: 36 months

– Mileage: 12,000 miles/year

– Down payment: $0–$2,000

These cars depreciate slowly and have low maintenance costs, making them excellent lease choices. Many automakers also offer lease specials on economy models to boost sales.

Midsize and Family Sedans

Vehicles like the Toyota Camry, Honda Accord, and Nissan Altima offer more space and features than compact cars, with slightly higher lease payments.

– Average monthly payment: $300–$450

– Typical lease term: 36 months

– Mileage: 12,000–15,000 miles/year

– Down payment: $0–$2,500

These sedans are popular among families and commuters who want reliability and comfort without the price tag of a luxury vehicle.

SUVs and Crossovers

SUVs are the most leased vehicle type in the U.S., thanks to their versatility, space, and safety features. Models like the Honda CR-V, Toyota RAV4, and Ford Escape fall into this category.

– Average monthly payment: $350–$550

– Typical lease term: 36 months

– Mileage: 12,000–15,000 miles/year

– Down payment: $0–$3,000

Luxury SUVs like the BMW X3, Mercedes GLC, or Audi Q5 can cost $600–$900 per month, depending on trim and options.

Luxury and Performance Vehicles

If you’re leasing a high-end car—think BMW, Mercedes-Benz, Audi, or Tesla—expect to pay a premium. These vehicles depreciate faster and come with higher maintenance and insurance costs.

– Average monthly payment: $600–$1,200+

– Typical lease term: 24–36 months

– Mileage: 10,000–12,000 miles/year

– Down payment: $2,000–$5,000+

While the monthly cost is higher, leasing a luxury car allows you to enjoy premium features and performance without the long-term commitment of ownership.

Electric and Hybrid Vehicles

Electric vehicles (EVs) like the Tesla Model 3, Chevrolet Bolt, or Hyundai Kona Electric are increasingly popular lease options. Many come with federal or state tax incentives that can reduce the effective lease cost.

– Average monthly payment: $300–$600

– Typical lease term: 36 months

– Mileage: 10,000–15,000 miles/year

– Down payment: $0–$3,000

EVs often have lower operating costs (no gas, less maintenance), which can offset higher lease payments. Some manufacturers also offer attractive lease deals to promote adoption.

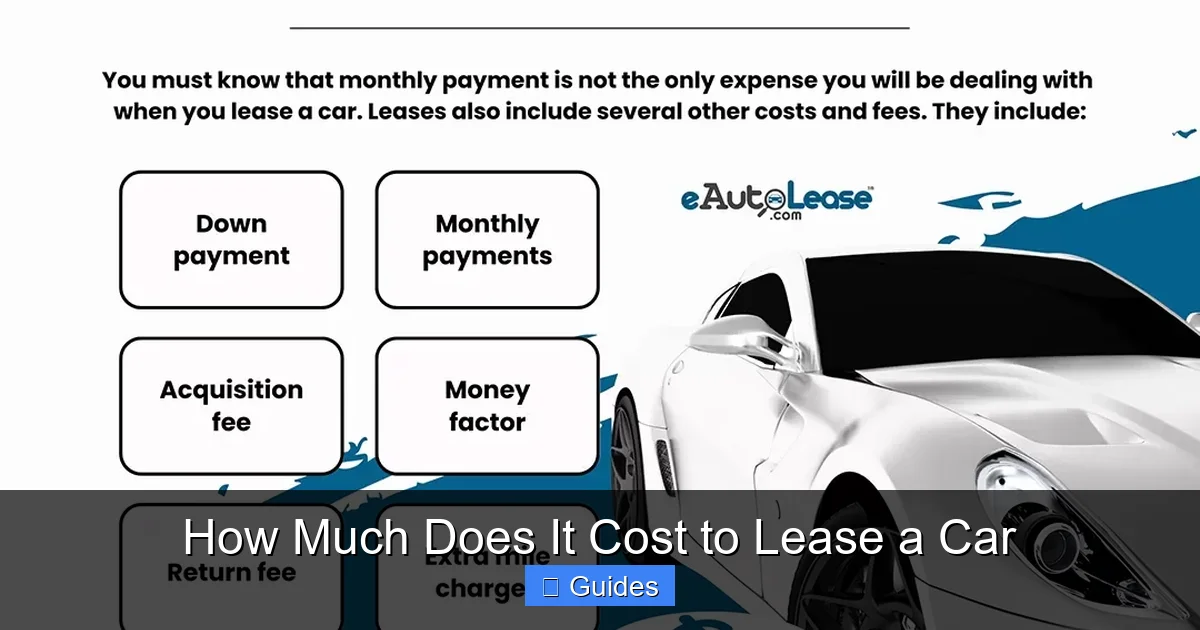

Hidden Costs and Fees to Watch Out For

While the monthly payment is the most visible cost, leasing a car comes with several additional fees and potential charges that can add up quickly if you’re not careful.

Acquisition Fee

Also known as the “bank fee” or “lease initiation fee,” this is a one-time charge (typically $500–$1,000) that covers the administrative costs of setting up your lease. It’s usually rolled into the lease, but you can sometimes pay it upfront to lower your monthly payment.

Disposition Fee

When your lease ends, the leasing company may charge a disposition fee (usually $300–$500) for cleaning, inspecting, and reselling the vehicle. This fee is often unavoidable, but some dealers waive it if you lease another car from them.

Excess Wear and Tear

At the end of your lease, the car will be inspected for damage beyond “normal wear and tear.” Scratches, dents, stained upholstery, or damaged tires could result in repair charges. To avoid surprises, take photos when you pick up the car and keep it well-maintained.

Early Termination Fees

Ending your lease early can be expensive. Most contracts charge a hefty fee—often several thousand dollars—to break the lease before the term ends. Some leases allow you to transfer the lease to another person (lease assumption), which can help reduce costs.

Taxes and Registration

Sales tax is usually applied to each monthly payment, and registration fees are typically due upfront. These vary by state, so check your local requirements. Some states also charge personal property tax on leased vehicles.

Gap Insurance

Most leases include gap insurance, which covers the difference between what you owe and the car’s value if it’s totaled or stolen. This is usually included in the lease cost, but confirm with your dealer.

How to Get the Best Lease Deal

Leasing doesn’t have to be expensive. With the right strategy, you can secure a great deal and keep your monthly payments low.

Negotiate the Capitalized Cost

Just like when buying a car, you can—and should—negotiate the price of the vehicle. The lower the capitalized cost (the price used to calculate depreciation), the lower your monthly payment. Research the invoice price and use competing offers to your advantage.

Time Your Lease Right

End-of-year sales, holiday promotions, and new model-year launches are prime times to find lease deals. Dealers often offer incentives like reduced money factors, waived fees, or cash credits to move inventory.

Check for Manufacturer Incentives

Automakers frequently run lease specials, especially on slow-selling models. These can include low or zero money factors, reduced down payments, or bonus cash. Visit manufacturer websites or ask your dealer about current offers.

Consider a Lease Buyout

If you love your leased car, you may have the option to buy it at the end of the lease for the predetermined residual value. This can be a smart move if the car has held its value well and you want to keep driving it.

Use a Lease Comparison Tool

Online tools like Edmunds, Leasehackr, or Cars.com allow you to compare lease offers from multiple dealers. These platforms show you the true cost of a lease, including fees and incentives, so you can make an informed decision.

Leasing vs. Buying: Which Is Cheaper?

One of the most common questions is whether leasing or buying is more cost-effective. The answer depends on your driving habits, financial goals, and how long you plan to keep the car.

Leasing Pros and Cons

Pros:

– Lower monthly payments than financing

– Drive a new car every 2–4 years

– Covered under warranty for most of the lease

– Minimal maintenance costs

Cons:

– No equity built

– Mileage and wear restrictions

– Fees at the end of the lease

– Ongoing payments with no ownership

Buying Pros and Cons

Pros:

– Own the car outright after paying it off

– No mileage limits

– Can customize or sell the car

– Lower long-term cost if kept for many years

Cons:

– Higher monthly payments

– Responsible for repairs after warranty

– Depreciation hits hardest in first few years

– Higher insurance costs for new cars

For drivers who want lower payments and enjoy driving new cars, leasing makes sense. But if you drive a lot, plan to keep a car for 10+ years, or want to build equity, buying may be the better choice.

Final Thoughts: Is Leasing Right for You?

So, how much does it cost to lease a car? As we’ve seen, the answer isn’t one-size-fits-all. Monthly payments typically range from $300 to $800, but the final cost depends on the vehicle, your credit, the lease term, and how much you’re willing to pay upfront.

Leasing offers many benefits—lower payments, newer technology, and fewer repair worries—but it’s not for everyone. If you love the idea of driving a new car every few years and can stay within mileage limits, leasing could be a smart financial move. Just be sure to read the fine print, negotiate the price, and avoid unnecessary fees.

Before you sign, ask yourself: Do I want to own this car? How many miles do I drive? Can I afford the upfront costs? Answering these questions will help you decide if leasing is the right choice—and ensure you get the best possible deal.

This is a comprehensive guide about how much does it cost to lease a car.

Key Takeaways

- Understanding how much does it cost to lease a car: Provides essential knowledge

Frequently Asked Questions

How much does it cost to lease a car per month?

The average monthly lease payment ranges from $300 to $800, depending on the vehicle type, lease term, and your credit score. Economy cars cost less, while luxury vehicles can exceed $1,000 per month.

Is it cheaper to lease or buy a car?

Leasing usually has lower monthly payments than buying, but you don’t build equity. Buying costs more upfront but can be cheaper in the long run if you keep the car for many years.

Can you negotiate a car lease?

Yes, you can negotiate the capitalized cost, money factor, and fees just like when buying a car. Research the car’s value and use competing offers to get the best deal.

What happens at the end of a car lease?

At the end of the lease, you return the car, pay any excess wear or mileage fees, and may be charged a disposition fee. You can also choose to buy the car or lease a new one.

Do you need good credit to lease a car?

While you can lease with fair credit, a higher credit score (720+) helps you qualify for lower interest rates and better lease terms. Poor credit may result in higher money factors and fees.

Can you lease a car with no money down?

Yes, many leases offer $0 down options, though this increases your monthly payment. Some deals also include first-month payment and registration fees due at signing.

At CarLegit, we believe information should be clear, factual, and genuinely helpful. That’s why every guide, review, and update on our website is created with care, research, and a strong focus on user experience.