Leasing a car offers lower monthly payments and the chance to drive a new vehicle every few years, but it comes with mileage limits and no ownership equity. This guide breaks down the key advantages and disadvantages to help you decide if leasing is the right choice for your needs.

In This Article

Key Takeaways

- Lower monthly payments: Lease payments are typically 30–50% lower than loan payments for the same vehicle, making luxury or high-end models more affordable.

- Drive a new car more often: Most leases last 2–4 years, so you can upgrade to the latest models with updated tech, safety features, and warranties.

- Warranty coverage included: New leased cars are usually covered by the manufacturer’s warranty, reducing out-of-pocket repair costs during the lease term.

- Mileage restrictions apply: Most leases limit annual mileage (e.g., 10,000–15,000 miles), and exceeding it results in costly per-mile fees.

- No ownership or equity: You don’t own the car at the end of the lease, so you gain no long-term value or ability to sell it.

- Fees and penalties for wear and tear: Excessive damage or modifications can lead to additional charges when returning the vehicle.

- Early termination costs: Ending a lease early often involves steep penalties, making it inflexible if your needs change.

📑 Table of Contents

Introduction: Is Leasing a Car Right for You?

So, you’re thinking about getting a new car—but instead of buying, you’re considering leasing. It’s a decision that’s becoming more popular, especially among drivers who want lower monthly payments or love driving the latest models. But like any financial choice, leasing a car comes with both perks and pitfalls. Whether you’re eyeing a sleek sedan, a rugged SUV, or a high-performance electric vehicle, understanding the advantages and disadvantages of leasing a car is crucial before signing on the dotted line.

Leasing is essentially renting a vehicle for a fixed period, usually 24 to 36 months, with the option to return it at the end of the term. Unlike buying, where you build equity and eventually own the car outright, leasing means you’re paying for the vehicle’s depreciation during your use—plus fees and interest. It’s a bit like renting an apartment: you get to enjoy the space and amenities, but you don’t own it, and there are rules to follow.

In this guide, we’ll walk you through everything you need to know about leasing a car—from the financial benefits and lifestyle perks to the hidden costs and long-term drawbacks. We’ll also share practical tips and real-life examples to help you make an informed decision. By the end, you’ll have a clear picture of whether leasing fits your budget, driving habits, and personal goals.

Advantages of Leasing a Car

Visual guide about Advantages and Disadvantages of Leasing a Car

Image source: autocartimes.com

Leasing a car isn’t just a trend—it’s a smart financial move for many drivers. While it’s not the right choice for everyone, the advantages of leasing a car can be compelling, especially if you value flexibility, lower costs, and access to the latest technology. Let’s dive into the top benefits that make leasing an attractive option.

Lower Monthly Payments

One of the biggest draws of leasing is the significantly lower monthly payment compared to buying. Since you’re only paying for the car’s depreciation during the lease term—not the full purchase price—your out-of-pocket cost each month is much more manageable. For example, leasing a $40,000 SUV might cost $450 per month, while financing the same vehicle could run $700 or more, depending on your down payment and loan terms.

This affordability opens the door to higher-end models you might not otherwise consider. Want a luxury sedan with premium sound, heated seats, and advanced driver-assist features? Leasing can make that dream car a reality without breaking the bank. It’s also a great option for people with tight budgets or those who prefer to keep more cash on hand for other expenses.

Drive a New Car Every Few Years

If you get bored easily or love being behind the wheel of the latest models, leasing is a perfect fit. Most leases last between 24 and 36 months, meaning you can upgrade to a new vehicle every two to three years. This gives you access to the newest safety tech, infotainment systems, fuel-efficient engines, and design updates—without the hassle of selling or trading in an old car.

For tech enthusiasts, this is a major perk. Imagine driving a car with over-the-air software updates, wireless Apple CarPlay, or even semi-autonomous driving features—all without committing to ownership. It’s like getting a smartphone upgrade every few years, but for your ride.

Warranty Coverage and Reduced Maintenance Costs

New leased vehicles are typically covered by the manufacturer’s bumper-to-bumper warranty for the entire lease term. That means if something goes wrong—whether it’s a faulty transmission or a glitch in the infotainment system—you’re usually covered at no extra cost. This peace of mind is a huge advantage, especially for drivers who don’t want to worry about unexpected repair bills.

Additionally, many leasing companies offer maintenance packages or include scheduled servicing in the lease agreement. Some even provide roadside assistance and loaner cars during repairs. This can save you time and money, and ensure your car stays in top condition throughout the lease.

No Hassle of Selling or Trading In

When you buy a car, eventually you’ll have to deal with selling it or trading it in—a process that can be time-consuming, stressful, and unpredictable. With leasing, the end of the term is simple: you return the car to the dealership, pay any applicable fees, and walk away. No need to haggle with private buyers, list your car online, or worry about depreciation.

This is especially helpful if you’re not great at negotiating or don’t have the time to manage a sale. It also eliminates the risk of getting less than expected for your trade-in value, which can happen when market conditions change.

Tax Benefits for Business Use

If you use your leased vehicle for business purposes, you may be eligible for tax deductions. The IRS allows businesses to deduct a portion of lease payments based on the percentage of business use. For example, if you drive your leased car 70% for work, you can deduct 70% of the monthly payments.

This can be a significant advantage for freelancers, consultants, or small business owners who rely on their vehicle for client meetings, deliveries, or site visits. Just be sure to keep detailed records of mileage and usage to support your deductions.

Disadvantages of Leasing a Car

Visual guide about Advantages and Disadvantages of Leasing a Car

Image source: cbselibrary.com

While leasing offers many benefits, it’s not without its downsides. The disadvantages of leasing a car can catch drivers off guard if they’re not fully prepared. From mileage limits to long-term costs, it’s important to weigh these drawbacks carefully before committing to a lease agreement.

Mileage Restrictions and Excess Fees

One of the most common frustrations with leasing is the mileage limit. Most leases cap annual mileage at 10,000, 12,000, or 15,000 miles. If you exceed this limit, you’ll be charged a per-mile fee—typically $0.10 to $0.25 per mile. For example, driving 18,000 miles in a year on a 12,000-mile lease could cost you an extra $1,500.

This makes leasing a poor choice for frequent travelers, commuters with long drives, or families who use their car for road trips. If you’re unsure about your annual mileage, it’s better to estimate high and pay a slightly higher monthly payment for a higher mileage allowance, rather than face surprise fees later.

No Ownership or Equity

When you lease, you’re essentially paying to use the car—not to own it. At the end of the lease, you don’t get to keep the vehicle or sell it for profit. This means you gain no equity, unlike with a car loan where each payment builds value in the asset.

Over time, this can make leasing more expensive than buying. For example, if you lease a car for three years, return it, and then lease another, you’re perpetually making payments without ever owning anything. In contrast, buying a car and keeping it for 8–10 years can result in significant long-term savings.

Fees for Wear and Tear

Leased cars must be returned in good condition. While normal wear and tear is expected, excessive damage—like deep scratches, dents, or stained upholstery—can result in additional charges. Dealerships use strict guidelines to assess condition, and even minor issues can add up.

For instance, a small tear in the driver’s seat or a cracked windshield might cost hundreds to repair. Some leases also charge for things like tire wear or paint damage. To avoid surprises, take photos of the car before and during the lease, and consider purchasing a wear-and-tear protection plan if available.

Early Termination Penalties

Life changes—jobs, relocations, family needs—and your car needs may change too. But ending a lease early is rarely easy or cheap. Most leases include early termination fees that can amount to thousands of dollars, often equivalent to several months of payments.

This lack of flexibility can be a major drawback if you need to move, switch vehicles, or simply can’t afford the payments anymore. Unlike buying, where you can sell the car and walk away, leasing locks you into a contract with financial consequences for breaking it.

Higher Long-Term Costs

While monthly payments are lower, leasing can cost more over time compared to buying. Since you’re always making payments and never building equity, the cumulative expense of leasing multiple cars over a decade can exceed the cost of buying and keeping one vehicle.

For example, leasing a $400/month car for 10 years totals $48,000—without owning anything. Buying the same car with a $600/month loan for 5 years, then keeping it for another 5 years with minimal costs, could save you thousands. If long-term savings are a priority, buying may be the better choice.

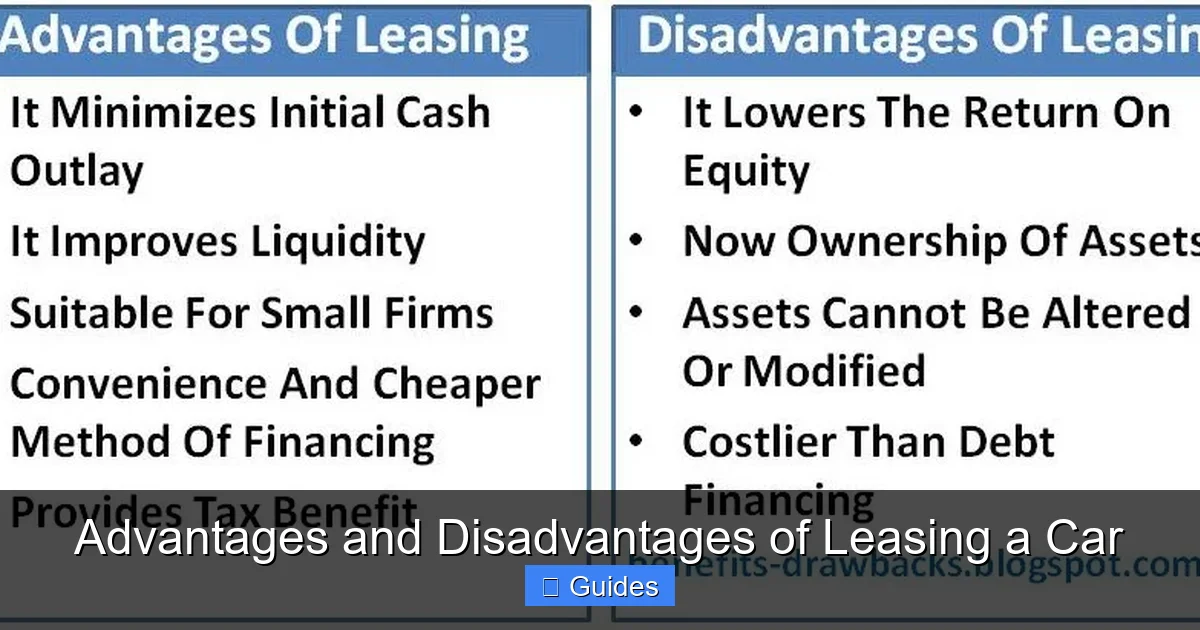

Who Should Lease a Car?

Visual guide about Advantages and Disadvantages of Leasing a Car

Image source: blogger.googleusercontent.com

Leasing isn’t one-size-fits-all. It works best for certain types of drivers who value specific benefits and can manage the limitations. Here’s who typically benefits most from leasing a car.

Low-Mileage Drivers

If you drive fewer than 12,000 miles per year—perhaps you work from home, have a short commute, or use public transit—leasing is a great fit. You’re less likely to exceed mileage limits and incur extra fees, making the lower monthly payments a real advantage.

Tech and Feature Enthusiasts

Love having the latest gadgets and safety features? Leasing lets you upgrade every few years to enjoy new tech without the hassle of selling your old car. Whether it’s adaptive cruise control, a premium sound system, or wireless charging, you’ll always be driving something current.

Business Professionals and Executives

Leasing is popular among professionals who want a reliable, stylish car for client meetings or business travel. The lower payments and tax deductions make it a smart financial move, and the ability to drive a new vehicle regularly projects a polished image.

People Who Hate Car Maintenance

If you dread oil changes, brake jobs, or unexpected repairs, leasing offers peace of mind. With warranty coverage and often included maintenance, you can focus on driving—not fixing.

Those Who Prefer Predictable Costs

Leasing provides fixed monthly payments and known end-of-lease costs. There are no surprises like depreciation drops or repair bills, making it ideal for budget-conscious drivers who want stability.

Tips for Getting the Best Car Lease Deal

If you’ve decided leasing is right for you, here are some practical tips to get the best deal and avoid common pitfalls.

Negotiate the Capitalized Cost

Just like with a purchase, the capitalized cost (the price of the car) is negotiable. Research the invoice price and aim to lease at or below it. A lower cap cost means lower monthly payments.

Watch Out for Fees

Leases often include acquisition fees, disposition fees, and documentation charges. Ask for a breakdown and try to reduce or waive unnecessary fees.

Choose the Right Mileage Allowance

Estimate your annual mileage accurately. If you’re close to a limit, pay a bit more upfront for a higher allowance to avoid excess charges later.

Consider a Shorter Lease Term

Shorter leases (24 months) often have lower interest rates and less depreciation, potentially saving you money. Just be aware that you’ll need to lease again sooner.

Read the Fine Print

Understand all terms, including wear-and-tear guidelines, early termination policies, and insurance requirements. Don’t sign until you’re confident you know what you’re agreeing to.

Conclusion: Weighing the Pros and Cons

Leasing a car offers undeniable advantages—lower payments, new technology, and hassle-free returns—but it also comes with real limitations like mileage caps, no ownership, and potential fees. The key is to match the decision to your lifestyle, driving habits, and financial goals.

If you drive moderately, love new features, and prefer predictable costs, leasing could be a smart, cost-effective choice. But if you put on high mileage, want long-term savings, or dream of owning your car outright, buying might be the better path.

Ultimately, the advantages and disadvantages of leasing a car depend on your personal situation. Take the time to compare lease offers, calculate total costs, and consider your long-term needs. With the right approach, leasing can be a rewarding way to enjoy driving without the long-term commitment of ownership.

Frequently Asked Questions

Is leasing a car cheaper than buying?

Leasing usually has lower monthly payments than buying, but it can cost more over time since you don’t build equity. It’s cheaper in the short term but may not be the most economical long-term option.

Can I negotiate a car lease?

Yes, you can negotiate the capitalized cost, money factor (interest rate), and certain fees. Research the vehicle’s value and be prepared to walk away if the deal isn’t right.

What happens at the end of a car lease?

You return the car to the dealership, pay any excess mileage or wear-and-tear fees, and may have the option to buy the vehicle or lease a new one.

Can I lease a used car?

Most leases are for new cars, but some dealerships and leasing companies offer certified pre-owned vehicles with lease options. These are less common and may have different terms.

Do I need full coverage insurance when leasing?

Yes, leasing companies require comprehensive and collision insurance with specific coverage limits to protect their asset. This is typically more than state minimum requirements.

Can I modify a leased car?

Modifications are generally not allowed unless approved by the leasing company. Any alterations must be reversed before returning the vehicle, or you may face charges.

At CarLegit, we believe information should be clear, factual, and genuinely helpful. That’s why every guide, review, and update on our website is created with care, research, and a strong focus on user experience.